Islamic Accounting in Islamic Boarding Schools Based on ISAK 35 (Case Study of Darul Hasanah Islamic Boarding School in Galang)

DOI:

https://doi.org/10.35891/40mqk793Keywords:

ISAK 35, boarding school accounting, financial transparency, accountability, Darul HasnahAbstract

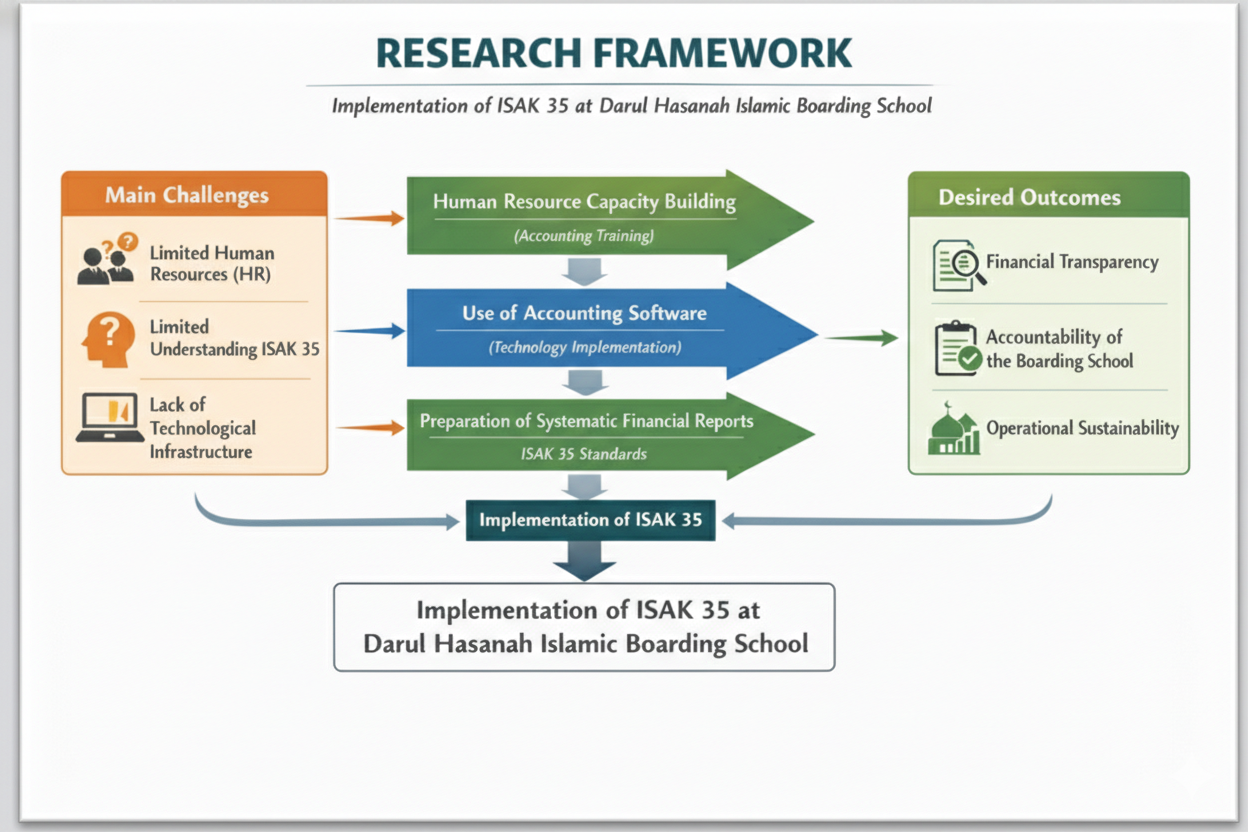

Purpose: This research examines the implementation of Financial Accounting Standards Interpretation (ISAK) 35 in Darul Hasanah Islamic Boarding School, aiming to analyze the challenges in its adoption and provide strategic recommendations for improving the school’s accounting system.

Design/Methodology/Approach: A qualitative case study approach was used, involving direct observations, in-depth interviews with financial managers and leadership, and document analysis. Data were analyzed using the Miles & Huberman method, which includes data reduction, presentation, and drawing conclusions.

Findings: The study identifies key challenges in implementing ISAK 35, including human resource limitations in accounting, a lack of understanding of ISAK 35, and insufficient technological infrastructure. The study recommends a phased strategy for implementation, focusing on HR training, the use of digital-based accounting software, and the preparation of more systematic financial reports.

Practical Implications: The findings suggest that adopting ISAK 35 can enhance financial transparency, strengthen trust from donors and the community, and ensure the sustainability of the boarding school’s operations.

Originality/Value: This research contributes to the literature on nonprofit accounting by exploring the application of ISAK 35 in Islamic boarding schools and offering evidence-based recommendations for improving accounting practices in these institutions.

Downloads

References

Abdurahim, A., Fatmawati, D., Saud, I. M., Budiarso, A. P., & Agustin, A. D. (2023). Implementation of the “SANTRI” Software at the MBS Wanayasa Islamic Boarding School. Proceeding International Conference of Community Service, 1(1), 168–174. https://doi.org/10.18196/iccs.v1i1.17

Adnan, M. I., Aliamin, A., & Mulyany, R. (2023). Accountability of Traditional Islamic Boarding School in Aceh. Jurnal Ilmiah Ekonomi Islam, 9(2), 1885. https://doi.org/10.29040/jiei.v9i2.8495

Ahyar, M. K. (2020). Tantangan Pondok Pesantren Menuju Lembaga Pendidikan Islam yang Akuntabel. JIFA (Journal of Islamic Finance and Accounting), 3(1). https://doi.org/10.22515/jifa.v3i1.2301

Alfie, A. A., & Triyoga, P. A. (2023). Analisis Laporan Keuangan Pondok Pesantren Berdasarkan Pedoman Akuntansi Pesantren dan ISAK 35. AKSES: Jurnal Ekonomi Dan Bisnis, 18(2). https://doi.org/10.31942/akses.v18i2.10209

Amelia Rizky Alamanda, Yudi Ahmad Faisal, & Runita Arum Kanti. (2022). Pelatihan Akuntansi Bagi Pengelola Pesantren Di Jawa Barat. J-ABDI: Jurnal Pengabdian Kepada Masyarakat, 1(10), 2675–2678. https://doi.org/10.53625/jabdi.v1i10.1615

Amelia, S., & Bharata, R. W. (2022). Analisis Penerapan ISAK No 35 Tentang Penyajian Laporan Keuangan Organisasi Nonlaba Pada Yayasan Hati Gembira Indonesia (Happy Hearts Indonesia). Akuntansiku, 1(4), 288–298. https://doi.org/10.54957/akuntansiku.v1i4.314

Ariwibowo, P., Heryadi, D., & Muzdalifah, M. (2023). Sharia Economic Transaction Academic Effectiveness on the Level of Community Well-Being. MALIA, 14(2), 235–254. https://doi.org/10.35891/ml.v14i2.3760

Arniati, A., Irianto, D., Utama, D. P., Halim, M. I., Slamet, M. R., Zelmiyanti, R., & Sinarti, S. (2021). Program Pendampingan Implementasi ISAK 35 Dengan Pembuatan Kebijakan Akuntansi Sebagai Pedoman Akuntansi Pondok Pesantren di Kota Batam. Jurnal Pengabdian Kepada Masyarakat Politeknik Negeri Batam, 3(2), 146–175. https://doi.org/10.30871/abdimaspolibatam.v3i2.3578

Arum, H. S., Rupita, N. E., Syahpawi, & Albahi, M. (2024). Maqasid Sharia As A Philosophical Foundation In Islamic Economic Policy Making. MALIA, 16(1), 28–43. https://doi.org/10.35891/ml.v16i1.5798

Asmedi, S., Stiawan, H., Syarifudin, S., Napisah, N., & Mundiroh, S. (2021). Peran Akuntansi Dalam Pengelolaan Wirausaha Pada Pondok Pesantren Lembaga Bina Santri Mandiri. DEDIKASI PKM, 2(3), 301. https://doi.org/10.32493/dedikasipkm.v2i3.10725

Auliyah, R., Nasih, M., & Agustia, D. (2025). Determinants of business success at Sunan Drajat Islamic Boarding School, east java Indonesia. Cogent Business & Management, 12(1), 2492828. https://doi.org/10.1080/23311975.2025.2492828

Carlitz, R. (2013). Improving Transparency and Accountability in the Budget Process: An Assessment of Recent Initiatives. Development Policy Review, 31(s1). https://doi.org/10.1111/dpr.12019

Dalimunthe, H., Nasution, I. R., Amelia, W. R., & Rizki, A. (2020). Improving the Quality of Financial Reports through Designing a Prototype of Islamic Boarding School Accounting in Medan, Indonesia. The International Journal of Business & Management, 8(1). https://doi.org/10.24940/theijbm/2020/v8/i1/BM2001-007

Dashkevich, N., Counsell, S., & Destefanis, G. (2024). Blockchain Financial Statements: Innovating Financial Reporting, Accounting, and Liquidity Management. Future Internet, 16(7). https://doi.org/10.3390/fi16070244

Deswita, S. (2023). Konstruksi Akuntansi dan Pelaporan Keuangan Aset Wakaf pada Pondok Pesantren Thawalib Tanjung Limau Berdasarkan PSAK No 112. Maro: Jurnal Ekonomi Syariah Dan Bisnis, 6(2), 260–270. https://doi.org/10.31949/maro.v6i2.7065

Dewy Titik Murtosyiah, Ade Irma Suryani Lating, M. Dliyaul Muflihin, & Nandha Nur Jagadhitawati. (2023). Accountability for Presentation of Financial Statements Based on ISAK No. 35 with Maqashid Syariah Perspective: Case Study on Khusnul Yaqin Wage Orphanage Foundation. Ta’amul: Journal of Islamic Economics, 2(2), 100–116. https://doi.org/10.58223/taamul.v2i2.85

Dharmawan, W. (2023). Penerapan Sistem Informasi Akuntansi Pengelolaan Keuangan Berbasis Website. Jurnal Sistem Informasi Akuntansi, 4(1), 74–83. https://doi.org/10.31294/justian.v4i1.1952

Fahamsyah, M. H., Achmad, L. I., Miharja, M. N. D., Wulandari, D. S., Novan, M., & Utomo, I. T. (2025). Digital Mediation in Institutional Theory: How Transactional Digitalization Bridges Pressures and Performance in Islamic Finance. MALIA, 17(1), 18–38. https://doi.org/10.35891/zbgjcc47

Fitriyani, Y., & Murtianingsih, M. (2023). Pelatihan Myob Accounting dalam Rangka Peningkatan Kompetensi Peserta Didik Jurusan Informatika Lembaga Pendidikan Wearnes Education Center Malang. Jurnal Pengabdian Masyarakat Tjut Nyak Dhien, 2(2), 1–11. https://doi.org/10.36490/jpmtnd.v2i2.598

Grigg, I. (2024). Triple Entry Accounting. Journal of Risk and Financial Management, 17(2). https://doi.org/10.3390/jrfm17020076

Harjawati, T., Sumiati, Aisjah, S., & Ratnawati, K. (2026). Integrated business strategies in Islamic boarding School-based businesses: A qualitative phenomenological study on human resource management, cooperation, marketing, production, and finance. Cogent Business & Management, 13(1), 2607801. https://doi.org/10.1080/23311975.2025.2607801

Hartoko, M. S. (2023). Implementasi ISAK 35 pada Organisasi Nirlaba. Wacana Equiliberium (Jurnal Pemikiran Penelitian Ekonomi), 11(02), 132–141. https://doi.org/10.31102/equilibrium.11.02.132-141

Islamic, G., Supriyono, Ishaq, M., & Dayati, U. (2024). Character education through philosophical values in traditional Islamic boarding schools. Kasetsart Journal of Social Sciences, 45(1), 31–42.

Laila, & Hanifah, L. (2024). Analisis Laporan Keuangan Pondok Pesantren Assalafi Al-Fithrah Surabaya berdasarkan ISAK 35. Jurnal Informatika Ekonomi Bisnis, 106–112. https://doi.org/10.37034/infeb.v6i1.803

Latief, D., Haliah, S. E., & Nirwana, S. E. (2020). Description of the Implementation of PSAK 45 and ISAK 35 in Mosque Financial Reporting Accounting (SSRN Scholarly Paper No. 3743296). Social Science Research Network. https://doi.org/10.2139/ssrn.3743296

Lotto, L. S. (1986). Qualitative Data Analysis: A Sourcebook of New Methods: Matthew B. Miles and A. Michael Huberman. Educational Evaluation and Policy Analysis, 8(3), 329–331. https://doi.org/10.3102/01623737008003329

Matei, M.-C., Abrudan, L.-C., & Abrudan, M.-M. (2024). Financial Perspectives on Human Capital: Building Sustainable HR Strategies. Sustainability, 16(4). https://doi.org/10.3390/su16041441

Muhibbin, Z., Soedarso, S., Harmadi, S. H. B., Saifulloh, Moh., Hamdan, F. Z. Z., Nisa, K., Rahmawati, D., & Mustofa, M. U. A. (2023). Pengembangan Santri Kreatif melalui Peningkatan Keterampilan Seni Islam dan Sumber Daya Pendukung di Pondok Pesantren Nurul Haromain 93 “Ribath Tahfidz Al-Qur’an Al-Fauzi.” Sewagati, 8(1), 1267–1275. https://doi.org/10.12962/j26139960.v8i1.906

Naz’aina, N., Raza, H., & Murhaban, M. (2023). Analysis of Accountability Determination in Bireuen Regency Islamic Boarding. International Journal of Social Service and Research, 3(1), 30–40. https://doi.org/10.46799/ijssr.v3i1.229

Novitasari, N., Agha, R. Z., Sixpria, N., Mahatmyo, A., & Redyanita, H. (2023). Pelatihan Dasar-Dasar Akuntansi Dan Pendampingan Penyusunan Laporan Keuangan Umkm Menggunakan Aplikasi Akuntansi Berbasis Cloud Si Apik. Jurnal Abdi Insani, 10(4), 2892–2902. https://doi.org/10.29303/abdiinsani.v10i4.1272

Nurkhin, A., Rohman, A., & Prabowo, T. J. W. (2024). Accountability of pondok pesantren; a systematic literature review. Cogent Business & Management, 11(1), 2332503. https://doi.org/10.1080/23311975.2024.2332503

Rahajeng, D. K., & Putri, B. K. M. (2024). Are We Accountable Enough? Exploring VBO Accounting, Reporting, and Governance in Indonesia’s Pesantren Landscape. In E. Lau, W. Paramita, K.-H. Tee, & L. M. Tan (Eds.), Economics and Finance Readings (pp. 195–215). Springer Nature. https://doi.org/10.1007/978-981-97-3512-9_11

Rahmasari, Y., & Pravitasari, D. (2023). Motivates that Influence Sharia Accounting Students to Become Auditors. MALIA, 15(1), 1–16. https://doi.org/10.35891/ml.v15i1.4257

Rodliyah, S., Djamhuri, A., & Prihatiningtias, Y. W. (2021). Revealing The Accountability of Nurul Haromain Islamic Boarding Schools: A Phenomenological Study. Jurnal Ilmiah Akuntansi Dan Bisnis, 16(2), 359. https://doi.org/10.24843/JIAB.2021.v16.i02.p12

Rofiah, N. H., Kawai, N., & Sudiraharja, D. (n.d.). Pesantren and inclusion: Bridging religion and disability in Islamic education in Indonesia. African Journal of Disability, 14(1), 1741. https://doi.org/10.4102/ajod.v14i0.1741

Ruci, D., & Prasetyo, H. (2022). Penerapan Pedoman Akuntansi Pesantren Di Pondok Pesantren Al I’tishom Kubu Raya. Jurnal Akuntansi Kompetif, 5(3), 406–422. https://doi.org/10.35446/akuntansikompetif.v5i3.1168

Sebri, S. H., Christian, A., & Aryadi Erwansah. (2023). Perancangan Aplikasi Administrasi Keuangan Sekolah Di Pondok Pesantren Modern Darussalam Menggunakan Metode Waterfall. JSK (Jurnal Sistem Informasi Dan Komputerisasi Akuntansi), 7(1), 26–29. https://doi.org/10.56291/jsk.v7i1.123

Sofanudin, A., & Atmanto, N. E. (2020). Penyebarluasan Best Practice Madrasah Ibtidaiyah. Open Science Framework. https://doi.org/10.31219/osf.io/ak2gw

Suhasto, Rb. I. N., Widodo, N. M., Amir, V., Pandowo, H., Christanti, Y. D., & Fikria, A. (2021). Implementasi Komputer Akuntansi Menggunakan Software Accurate di Lingkungan Yayasan Pendidikan dan Pondok Pesantren Subulul Huda Kembangsawit Kebonsari Madiun. DIKEMAS (Jurnal Pengabdian Kepada Masyarakat), 5(1). https://doi.org/10.32486/jd.v5i1.767

Sulistiani, D. (2020). Akuntansi Pesantren Sesuai SAK ETAP dan PSAK 45 dalam Penyusunan Laporan Keuangan Pesantren. AKTSAR: Jurnal Akuntansi Syariah, 3(1), 31. https://doi.org/10.21043/aktsar.v3i1.7198

Supriyati, S., & Bahri, R. S. (2020). Model Perancangan Sistem Informasi Akuntansi Laporan Keuangan Pondok Pesantren Berbasis SAK ETAP. Is The Best Accounting Information Systems and Information Technology Business Enterprise This Is Link for OJS Us, 4(2), 151–165. https://doi.org/10.34010/aisthebest.v4i02.2749

Sutrisno, C. R., Ilmiani, A., Al Farisi, S., Kushemanto, A., Prasetya, N. A., & Khoiri, H. (2025). Improving Financial Management in Islamic Boarding Schools: Socialization of Accounting Guidelines and Financial System Application Tutorial. Community Development Journal, 9(1), 502–510. https://doi.org/10.33086/cdj.v9i1.7176

Syukri, M., Fitri, S. M., & Syafhariawan, H. (2023). Analisis Pelaporan Keuangan Pondok Pesantren Al-Muthmainnah Berdasarkan Pedoman Akuntansi Pesantren. Jurnal Economina, 2(1), 1175–1183. https://doi.org/10.55681/economina.v2i1.266

Ulfi, I., & Rizaldy, M. R. (2024). A Review on Islamic Corporate Governance Research in Islamic Financial Institution. MALIA, 15(2), 126–146. https://doi.org/10.35891/ml.v15i2.5091

Wati, R., Ardini, L., & Fidiana, F. (2022). The Implementation of Spiritual and Financial Accountability in Islamic Boarding School. Al-Uqud : Journal of Islamic Economics, 6(1), 101–114. https://doi.org/10.26740/aluqud.v6n1.p101-114

Wijaya, I. S., Ridho, M., Hidayati, D. L., & Mahdi, M. (2024). Utilization of Digital Technology in Islamic Boarding Schools: A Case Study in Samarinda. Lentera: Jurnal Ilmu Dakwah Dan Komunikasi, 140–153. https://doi.org/10.21093/lentera.v7i2.7390